UK Electricity Generator Levy Rises to 55% from 1 July 2026: What Generators Must Know

HMRC's June 2026 policy paper confirms the Electricity Generator Levy rate increases from 45% to 55% on receipts from 1 July — with time-apportioned accounting periods, a £82.61 benchmark, and EGL extension beyond 2028.

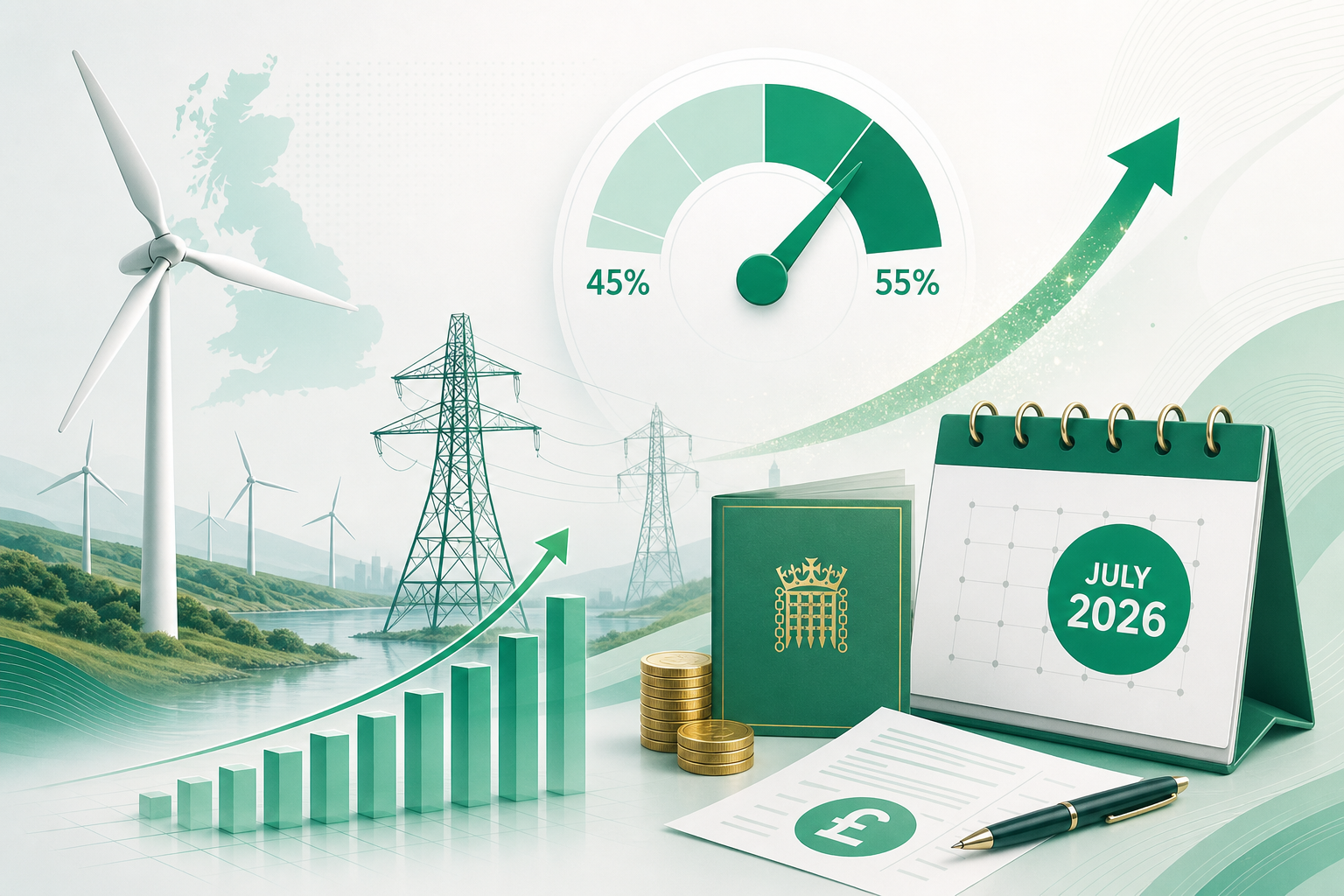

From 1 July 2026 the UK Electricity Generator Levy (EGL) rate rises from 45% to 55% on exceptional receipts from wholesale electricity production. HMRC published a policy paper on 17 June 2026 confirming transitional rules, benchmark pricing, and the government's intention to extend the levy beyond its original 2028 end date.

The EGL targets windfall revenues earned by renewable and nuclear generators when wholesale prices exceed a benchmark — typically when gas sets the marginal price. For energy companies and their tax teams, the July rate change affects corporation tax cash flow, quarterly instalment planning, and how receipts are split across straddling accounting periods.

How the 55% rate applies from 1 July

The higher rate applies to receipts attributable to electricity generated on or after 1 July 2026 — not to receipts invoiced or received on that date. Generation timing drives the rate, which matters for long-term power purchase agreements and settlement lag.

EGL is charged on receipts above the benchmark price within a qualifying period that aligns with a corporation tax accounting period. For 2026–27 the benchmark is £82.61 per MWh, indexed to CPI from 1 April 2026. Only exceptional receipts above that threshold attract the levy.

The government announced the increase in a Written Ministerial Statement on 21 April 2026, citing sustained high wholesale prices linked to geopolitical energy disruption. New renewable investments remain outside scope, preserving the original carve-out for greenfield projects.

Straddling periods and quarterly instalments

Where a qualifying period spans 1 July 2026, receipts must be apportioned on a time basis. Amounts attributable to generation before 1 July stay at 45%; amounts from 1 July onwards are charged at 55%. Document your apportionment methodology before filing — HMRC expects consistent treatment across EGL and corporation tax returns.

Large and very large companies paying corporation tax by quarterly instalments do not need to reflect the increased EGL liability in payments due before Royal Assent. The additional charge is included in the first instalment due after Royal Assent, with interest applied accordingly.

Finance teams should model the blended effective rate for the current accounting period rather than assuming a flat 55% from 1 July on all receipts. Mixed-rate periods require separate EGL calculations for each portion.

Extension beyond 2028 and policy context

Alongside the rate increase, the government confirmed it intends to extend the EGL past its scheduled conclusion in March 2028. Legislation for the extension will follow in due course — generators should not assume the levy ends on the original timetable.

The EGL was introduced in Finance (No. 2) Act 2023 from 1 January 2023 as a temporary charge on exceptional generation receipts. The June 2026 policy paper amends section 279(1) to set the 55% rate and provides the straddling-period transitional rule.

Northern Ireland generators within the UK wholesale market are in scope where EGL conditions are met. Cross-border electricity trading and benchmark price mechanics follow the same UK-wide rules.

Practical steps for energy businesses

Recalculate EGL forecasts for the current accounting period using time-apportioned generation data from 1 July. Update quarterly instalment models to reflect the post-Royal Assent payment timing for large companies.

Review power purchase agreement and hedging documentation — contractual settlement dates may differ from generation dates used for EGL apportionment. Align billing systems with generation timestamps where possible.

FinnAccountings tracks corporation tax and industry-specific levy forecasts from your ledger — start a free trial to model EGL liability alongside your main CT position.

Sources & references

This article draws on official guidance and publications from the sources below.

- 1.Increase in the rate of the Electricity Generator Levy

HM Revenue & Customs · Accessed 2026-07-03

- 2.Amended rate of the Electricity Generator Levy — 2026 to 2027

GOV.UK · Accessed 2026-07-03

- 3.Electricity Generator Levy: rate increase from 1 July 2026

HM Revenue & Customs · Accessed 2026-07-03

Put this advice into action

FinnAccountings automates bookkeeping, tax, and VAT for Ireland and the UK.

Start Free Trial