PAC Report: US Pillar 2 Exemption Cuts UK Minimum Tax Revenue by £600m a Year

On 10 July 2026 the Public Accounts Committee warned HMRC must tackle £21bn of international profit-shifting risk — and confirmed the US OECD deal reduces expected UK Pillar 2 receipts from £2.2bn to £1.6bn annually.

On 10 July 2026 the House of Commons Public Accounts Committee published its report on large business tax compliance, highlighting that around £21 billion of the £70.1 billion under HMRC investigation in 2025 relates to international risks including profit shifting — even as the OECD Pillar 2 global minimum tax regime takes effect.

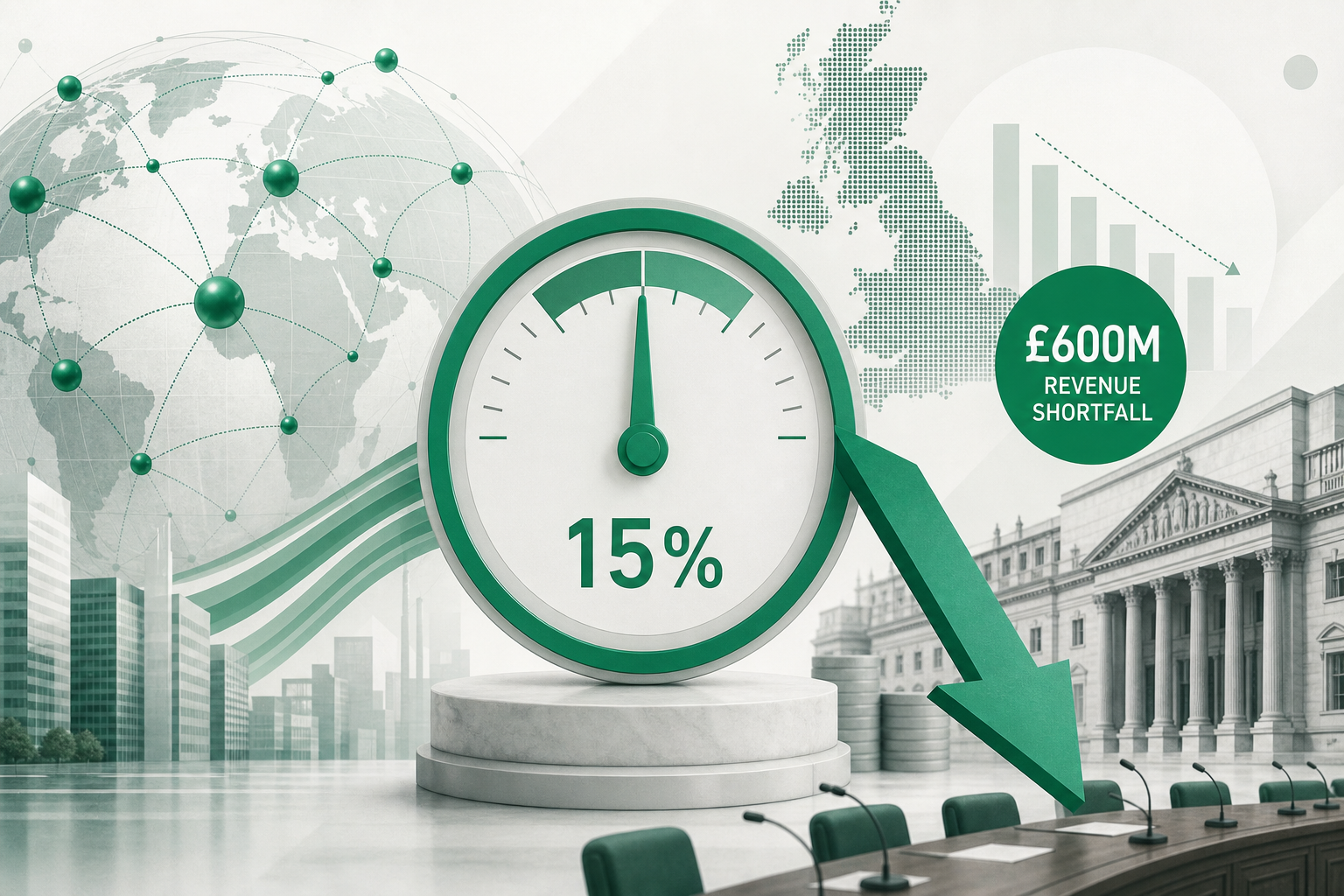

The committee's starkest finding for fiscal planners: HMRC estimates the US exemption from Pillar 2 will reduce UK top-up tax receipts by £600 million a year, cutting expected annual revenue from £2.2 billion to £1.6 billion. For multinational groups and their advisers, the report also raises enforcement timelines, unused special measures powers, and IT transformation delivery.

How the US deal shrinks Pillar 2 receipts

Pillar 2 introduces a 15% global minimum effective corporate tax rate for multinational groups with consolidated revenue above €750 million. The UK implemented multinational top-up tax and domestic top-up tax from accounting periods beginning on or after 31 December 2023.

In January 2026 the United States negotiated an OECD agreement exempting US-headquartered companies from Pillar 2 application. HMRC told the PAC this reduces the additional tax the UK expected to collect by about £600 million annually — a 27% shortfall against the original £2.2 billion projection.

Nicole Newbury, HMRC director of large business compliance, confirmed the figure to the committee. The PAC warns the UK still risks significant tax leakage through cross-border profit diversion, and HMRC must improve transparency on how groups comply with minimum tax rules in light of the US carve-out.

£21 billion of international compliance risk

HMRC's large business investigations covered £70.1 billion of tax under consideration in 2025. Approximately £21 billion — nearly 30% — relates to international risks, including transfer pricing, permanent establishment disputes, and profit allocation across jurisdictions.

Despite this exposure, the PAC found HMRC has never used its special measures regime powers, available since 2016, to intensify scrutiny of the worst-offending large businesses. The legislative threshold may be set too high even where companies are aggressively avoiding tax.

HMRC also makes limited use of prosecution powers for failing to prevent the facilitation of corporate tax evasion. The committee argues this undermines credibility when HMRC seeks further enforcement powers elsewhere.

Investigation delays and IT transformation

Completed large business compliance investigations in 2024–25 took an average of 17 months to conclude. Cases involving litigation averaged 97 months — over eight years — before resolution, delaying cash collection and creating uncertainty for both HMRC and taxpayers.

HMRC received £1.6 billion for new IT infrastructure in the 2025 Spending Review, with much of its compliance improvement strategy resting on the Transformation Roadmap. The PAC is not yet convinced the programme will deliver measurable benefit for the Large Business Directorate.

HMRC secured an additional £14.9 billion from large businesses through compliance activity in 2024–25, with the Large Business Directorate generating £15.8 billion that would otherwise have been lost. The PAC acknowledges strong yield but demands faster case resolution and clearer public reporting.

What multinationals should do now

Groups with US parent entities should model Pillar 2 liability under both the original OECD framework and the US exemption scenario. Filing obligations for UK top-up tax returns and GloBE information returns remain — HMRC's transitional approach waives late filing penalties only until 1 August 2026.

Document transfer pricing policies, substance in UK entities, and Pillar 2 safe harbour elections before HMRC enquiry. The PAC report signals continued scrutiny of profit shifting even where minimum tax rules partially bite.

FinnAccountings tracks Pillar 2 and transfer pricing filing deadlines across UK and Irish entities — start a free trial to keep multinational compliance calendars aligned as international rules evolve.

Sources & references

This article draws on official guidance and publications from the sources below.

- 1.HMRC must better tackle large tax risk of multinationals diverting profits across borders

Public Accounts Committee · Accessed 2026-07-11

- 2.How to report Pillar 2 Top-up Taxes

HM Revenue & Customs · Accessed 2026-07-11

- 3.£600m tax revenue vanishes: How US deal punched a hole in UK's global minimum tax plan

Reuters / upday · Accessed 2026-07-11

Put this advice into action

FinnAccountings automates bookkeeping, tax, and VAT for Ireland and the UK.

Start Free Trial