HMRC Proposes Automated Bank Deductions for Lower-Value Tax Debts Up to £10,000

HMRC's June 2026 consultation proposes extending Direct Recovery of Debts to collect up to £10,000 in persistent non-engagement cases via automated monthly instalments from UK bank accounts — consultation closes 28 August 2026.

On 23 June 2026 HM Revenue & Customs opened a consultation on extending its Direct Recovery of Debts (DRD) powers to recover lower-value tax debts from customers who persistently fail to engage. The measure was announced at Spring Statement 2025 and forms part of HMRC's wider push to close the estimated £59.2 billion tax gap.

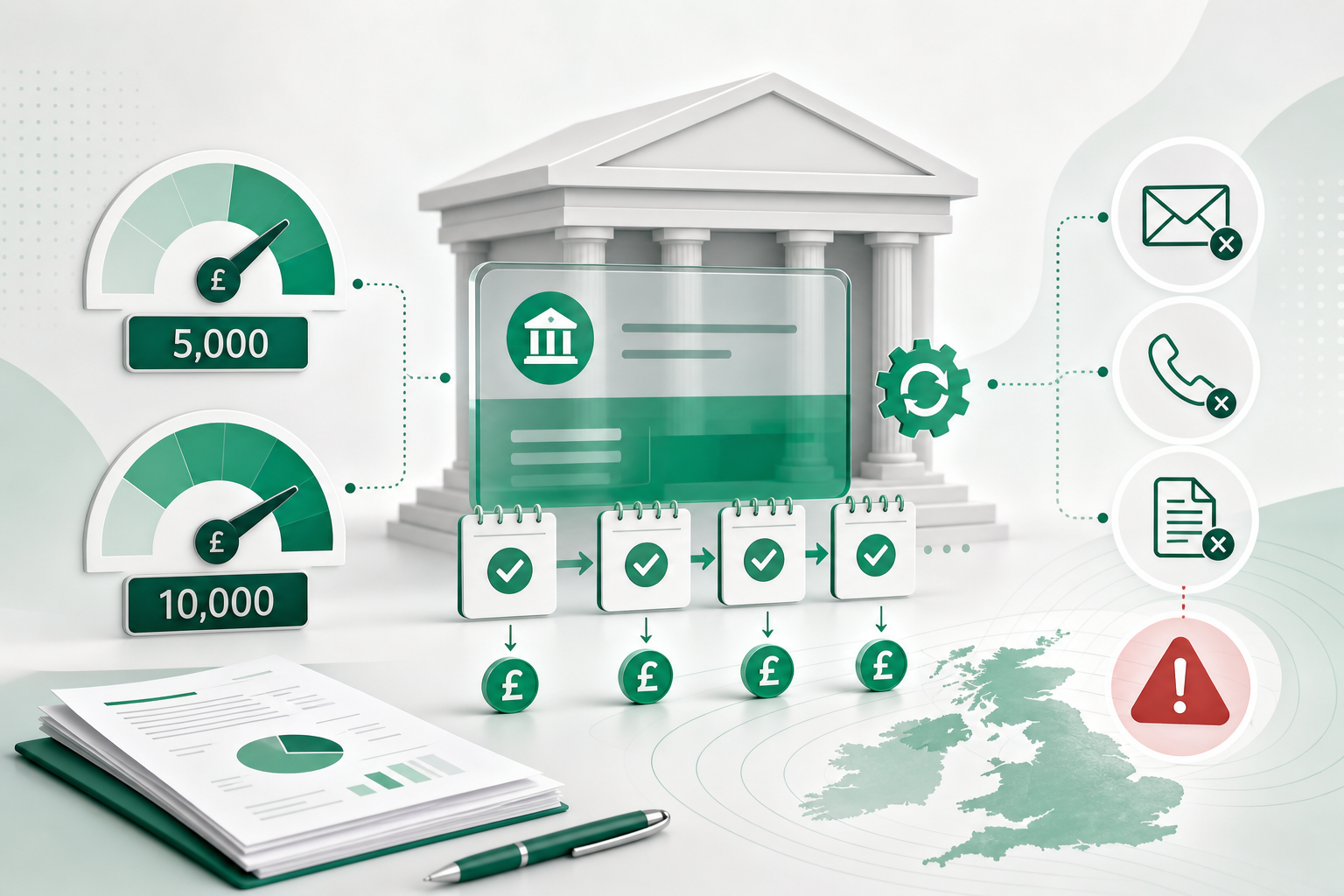

Unlike existing DRD — which takes a one-off lump sum and leaves at least £5,000 in the taxpayer's account — the proposed power would deduct affordable monthly instalments automatically across all tax regimes where total debt falls within expected limits of £5,000 for individuals and £10,000 for businesses.

Why HMRC wants a new collection tool

Around 90% of customers pay tax in full and on time, but approximately £100 billion of tax becomes debt each year. HMRC resolves over 95% by value through reminders, Time to Pay plans, and existing enforcement — yet a persistent minority ignores all contact.

Each year more than 750,000 lower-value debts collectively worth over £2 billion return from debt collection agencies because the customer cannot be reached or will not pay. Court action and Taking Control of Goods involve fixed costs that make them uneconomic for high volumes of small debts.

Internal analysis suggests 4.8 million individuals and companies hold debts at or below £5,000 (individuals) or £10,000 (businesses), representing roughly 11.5 million debts totalling around £4 billion — the pool the new power targets.

How automated instalment recovery would work

HMRC would use automated processes to deduct monthly instalments directly from UK bank or building society accounts only after standard collection routes — reminders, phone calls, debt collection agency referral — are exhausted.

Customers receive advance notification and a final opportunity to pay or contact HMRC before deductions begin. Instalment amounts would follow affordability principles similar to existing Time to Pay agreements, typically completing in around 14 months.

The power applies to total tax debt across all regimes — income tax, VAT, PAYE, and corporation tax combined — not individual liabilities in isolation. HMRC may roll out through a phased test-and-learn approach.

Safeguards and who is excluded

The consultation proposes manual review by trained staff where vulnerability or financial hardship indicators appear, with ability to divert cases away from automation. Customers retain rights to object, appeal, complain, and seek independent review or tribunal oversight.

HMRC's existing processes to identify customers requiring extra support would apply before enforcement. Innocent errors and customers in genuine temporary difficulty who engage early remain outside the target group — the policy focuses on persistent non-engagement.

Financial institutions would implement deduction instructions on HMRC's authority. The consultation seeks views on operational burden for banks and building societies as well as proportionate debt value limits.

What businesses and agents should do

Respond to the consultation by 28 August 2026 at [email protected] if you represent small businesses, vulnerable taxpayers, or financial institutions affected by automated deductions.

Ensure clients respond to HMRC correspondence promptly — the proposed power activates only after persistent non-engagement. Set up Direct Debit for VAT and PAYE where possible to avoid accidental debt accumulation from missed deadlines.

FinnAccountings sends payment reminders and reconciles HMRC liabilities against your ledger before they become enforceable debts — start a free trial to stay ahead of collection action.

Sources & references

This article draws on official guidance and publications from the sources below.

- 1.Tackling lower value tax debts

HM Revenue & Customs · Accessed 2026-07-11

- 2.Proposals to tackle lower value tax debts

GOV.UK · Accessed 2026-07-11

- 3.HMRC targets lower value tax debt

ICAEW · Accessed 2026-07-11

Put this advice into action

FinnAccountings automates bookkeeping, tax, and VAT for Ireland and the UK.

Start Free Trial